In the world of corporate finance, not all moves are as transparent as they seem. Recent developments surrounding Xerox’s massive $550 million share buyback raises more questions than answers, particularly when delving into the nuances of the transaction.

On the surface, Xerox’s board champions this: “Our decision to repurchase shares is reflective of the confidence we have in our business, our strategy and our ability to improve Xerox profitability and cash performance,” said Steve B.

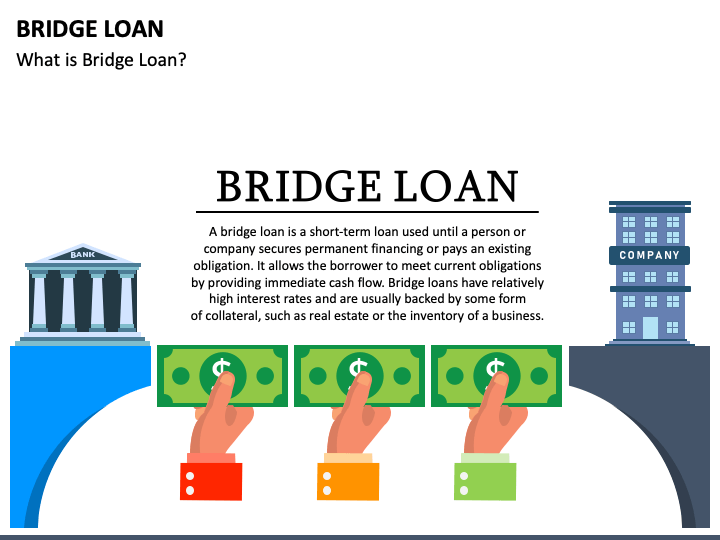

However, evidence suggests a more intricate web. For a company that reportedly lacks the liquidity to execute such a large buyback, the immediate question is, “How?” Enter the bridge loan—a short-term financial lifeline.

But there’s a catch! Xerox’s bridge loan comes courtesy of Jefferies, an institution with long-standing ties to Icahn. Intriguingly, Jefferies’ involvement in an alleged Ponzi scheme with Icahn, as documented by Hindenburg Research, thickens the plot. Regardless of the motivations, this buyback carries significant financial ramifications for Xerox.

*an increase in liabilities, given the borrowed funds, will strain the company’s financial health; *taking on debt translates to added interest expenses, weighing down on net income; *With fewer shares on the market, there might be a temporary boost in Earnings Per Share (EPS), painting a rosier picture of profitability;

However, the board of directors just declared a quarterly dividend of $0.25 per share on Common Stock, so no temporary boost at all. Only time will reveal the full impact of this maneuver, but for now… just look at Xerox share price.